HELOC vs Cash Out Refinance: Which Wins?

Compare heloc vs cash out refinance on rates, payments, fees, and flexibility so you can choose the smarter equity option for your home.

When Should I Refinance My Mortgage?

When should I refinance? Learn the right time to lower your rate, payment, or tap equity without hurting credit in Short Pump and Richmond.

Cash Out Refinance Requirements Explained

Learn cash out refinance requirements, credit scores, equity, DTI, appraisal rules, and how Richmond area homeowners qualify with a soft pull.

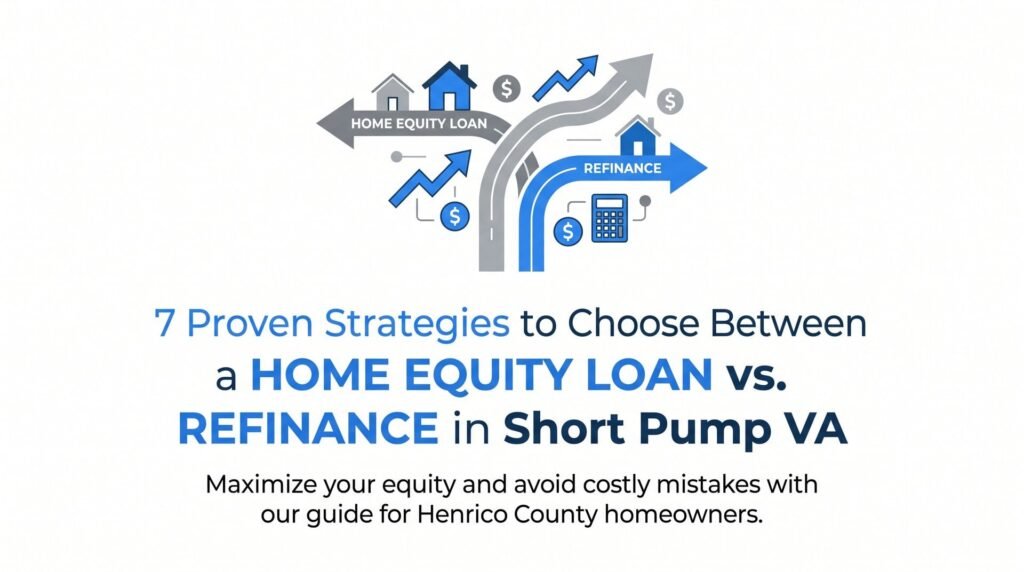

7 Proven Strategies to Choose Between a Home Equity Loan vs. Refinance in Short Pump VA

Short Pump and Henrico County homeowners with $100,000–$250,000 in built-up equity face a critical choice between a home equity loan vs. refinance—and picking the wrong option can cost tens of thousands of dollars. This guide breaks down seven proven strategies to help Virginia homeowners evaluate both options based on their current rate, financial goals, and long-term cost.

Why Choose Short Pump Mortgage for Your Loan

Why Choose Short Pump Mortgage? Get soft-pull pre-approval, 500+ lenders, lower rates, and local broker guidance in Short Pump VA.

Bank Statement Loan Virginia: What Self-Employed Buyers in Short Pump Need to Know

Self-employed buyers in Short Pump, VA who’ve been denied by retail banks due to tax return income can qualify for a **bank statement loan Virginia** lenders offer through Non-QM programs, using 12–24 months of actual deposits instead of W-2s or tax returns. With Short Pump median home prices between $475,000–$550,000 and homes moving in under 30 days, working with an independent mortgage broker provides access to these flexible products that most retail banks simply don’t offer.

Home Equity Line of Credit Richmond VA: What Short Pump Homeowners Need to Know in 2026

Short Pump homeowners in 23233 are sitting on six figures of untapped equity as 2026 median prices hit $520,000–$527,000, making a home equity line of credit Richmond borrowers can access through a wholesale broker — rather than a retail bank — a potentially significant money-saving decision. This guide breaks down HELOC qualification rules, CLTV limits, variable rate risks, and why lender choice matters more than most homeowners realize.

7 Low Down Payment Mortgage Options That Actually Work in Short Pump VA

Short Pump’s $520,000+ median home price doesn’t have to mean $100,000 at closing — seven proven low down payment mortgage options, including 0% VA loans and 3.5% FHA programs, give qualified buyers in 23233 and western Henrico County a realistic path to homeownership without draining savings.

How to Refinance Without Affecting Your Credit Score: A Step-by-Step Guide for Short Pump Homeowners

Short Pump homeowners can refinance a $525,000 home from 7.25% to 6.50%—saving $214/month—without damaging their credit score by using soft-inquiry pre-approvals and federal 45-day rate-shopping protections that bundle multiple mortgage pulls into one. This step-by-step guide shows western Henrico borrowers exactly how to refinance without affecting credit while comparing real rates across hundreds of lenders before authorizing a single hard inquiry.

7 Proven Strategies to Get Approved as a Self-Employed Mortgage Borrower in Short Pump, VA

Self-employed borrowers in Short Pump, Glen Allen, and Goochland often face mortgage denials despite strong income, because traditional lenders rely on tax returns that understate earnings after deductions. This guide covers 7 proven strategies—including bank statement loans, DSCR financing, and working with a specialized mortgage lender for self-employed borrowers—to help business owners qualify based on actual cash flow rather than taxable income.